How to Open a Bank Account in Japan as a Foreigner (2026): No 6-Month Wait

CEO / Native Japanese Expert

Updated on: June 21, 2026

Essentials

How this guide is checked

Updated against official, partner, and reviewed site evidence where available.

Last updated: June 21, 2026

Official or partner facts are separated from practical notes.

Prices, screening, documents, and rules can change.

Some next-step links may be monetized.

Needs review: Approval, visa/tax/legal, availability, and campaign terms are not guaranteed. Confirm on the official or partner page.

Recommended next step

Before opening a bank account, prepare phone number, transfers, and ID setup

Bank setup often stalls at SMS verification and moving money, so these actions stay close to the decision point.

Before applying, check the destination page for current eligibility, from-abroad or domestic application options, required documents, and support languages.

This page contains affiliate links. We may earn a commission from purchases or sign-ups, at no extra cost to you. Learn more

Send to Friends (Summary)

- •How to open a bank account in Japan as a foreigner — even within 6 months of arrival. The bank that accepts newcomers, the 4 documents you need, app-based steps in English, and how to avoid the non-resident fee trap.

Great for LINE / WhatsApp sharing

Quick answer: For most foreigners who have been in Japan for less than 6 months, the fastest way to open a bank account is Japan Post Bank (Yucho) via the "Yucho Tetsuzuki App" — you need a Residence Card with your address printed on the back, a Japanese phone number in your own name, and a visa with 3+ months remaining. If you are employed in Japan, SBI Shinsei Bank can waive the 6-month rule with proof of employment. For sending money, use Wise instead of bank transfers to avoid "non-resident" fees.

Last updated: 2026-06-11

Which bank should you choose? (30-second decision)

- Student / unemployed, in Japan less than 6 months → Japan Post Bank (Yucho) via the app (visa with 3+ months remaining)

- Employee, in Japan less than 6 months → SBI Shinsei Bank with proof of employment, or Yucho

- In Japan more than 6 months → Rakuten Bank, SBI Shinsei, and most other banks open up

- Need to move money now → Use Wise — accounts opened in your first 6 months are "non-resident" accounts with expensive transfers

Opening a bank account is one of the first steps in our First Week in Japan Checklist — right after getting a SIM card with a Japanese phone number.

Introduction: Why is Opening a Bank Account in Japan So Hard?

"Moving to Japan, the first challenge wasn't the language. It was opening a bank account."

This is a sentiment shared by many foreigners we interviewed. You may have already experienced being told "No" at a bank counter. Or perhaps you are overwhelmed by a mountain of complex paperwork.

Rest assured, it's not because of your Japanese ability. The Japanese banking system operates under strict "Foreign Exchange Act" regulations to prevent money laundering.

However, with the right knowledge and strategy, you can break through this wall. This guide presents the "only correct answer" on which bank to choose for the fastest approval, based on real reviews from senior expats.

What You Will Learn

- ✅ The Verdict: The "only bank" where you can open an account even if you've been in Japan for less than 6 months.

- ✅ Real Talk: App vs. Counter – which is better? (Based on user reviews)

- ✅ The Hack: How to get a phone number without a bank account (the chicken-and-egg problem).

- ✅ Money Saving: How to avoid "Non-Resident Fees" when transferring money.

⚠️ ID rule change (since December 1, 2025) The paper Health Insurance Card is no longer accepted as a valid ID at banks. Bring your Residence Card (and My Number Card if you have one) instead.

The Biggest Hurdle: The "6-Month Rule" Explained

90% of rejections at bank counters are due to this rule.

1. Why "6 Months"?

Under Japanese law (Foreign Exchange and Foreign Trade Act), foreigners who have been in Japan for less than 6 months are defined as "Non-Residents." Since standard savings accounts at Japanese banks are designed for "Residents," legally, they cannot offer regular accounts to Non-Residents (or can only offer accounts with limited functions).

2. Are There Exceptions?

Yes. There are two main routes.

Route A: Japan Post Bank (Yucho Ginko)

- Condition: You must have at least 3 months remaining on your visa.

- Feature: The most flexible bank for foreigners in Japan. Even immediately after arrival, if you have a visa of 3 months or more, the probability of opening a "General Savings Account" is extremely high.

Route B: Proof of Employment (SBI Shinsei Bank, etc.)

- Condition: You can prove you are working for a company in Japan (Employee ID, Employment Contract).

- Feature: Even if it's less than 6 months, there is a special exception where you are treated as a "Resident" if you are actually working in Japan.

Quick Verdict: Which Bank is for You?

| Your Situation | Recommended Bank | Success Rate |

|---|---|---|

| Student / Unemployed (< 6 months) | Japan Post Bank (Yucho) | ⭐⭐⭐⭐⭐ |

| Employee (< 6 months) | SBI Shinsei Bank or Yucho | ⭐⭐⭐⭐ |

| Anyone (> 6 months) | Rakuten Bank, SBI Shinsei, etc. | ⭐⭐⭐⭐⭐ |

The "4 Sacred Treasures": Required Documents Checklist

Before going to the bank, ensure you have these four items. Missing even one will result in being sent home immediately.

1. Residence Card (Zairyu Card) [Mandatory]

This is the core of your ID.

- Crucial Check: Is your "Current Address" printed on the back? If your address is undecided immediately after entry, you cannot open an account. The absolute first step is to register your address at the City Hall and get it printed on the back of the card.

2. Japanese Phone Number [The Biggest Bottleneck]

Many foreigners stumble here. Banks require a "Japanese mobile number (090/080/070) where you can be contacted."

- 050 Numbers (IP Phone)? Mostly NG. They don't support SMS verification, failing security requirements.

- Friend's Number? NG. It must be in your own name.

Solution: Get a SIM card you can contract without a bank account first. These are the "keys" to opening a bank account.

💡 Recommended SIMs Without a Bank Account Only the following two companies can solve the "No bank, no phone / No phone, no bank" dilemma.

- Mobal SIM: No credit card required. Contract with just a passport.

- GTN Mobile: Specialized for foreigners. Convenience store payment OK.

3. Certificate of Residence (Juminhyo)

Some banks (especially when opening at a counter) require this. Follow the bank's instructions regarding whether to include your My Number (Individual Number).

- Tip: If you have a My Number Card, you can print this at a convenience store 24/7.

4. Hanko (Personal Seal)

"Do I still need a stamp?" — The situation is changing.

- App / Online Banks: Basically not required (Signature or Face ID).

- Japan Post Bank (Counter): Often required.

- Advice: Avoid 100-yen shop stamps (they might be rejected for bank registration).

Top 3 Banks Comparison: Which One Fits You?

1. Japan Post Bank (Yucho Bank)

- Verdict: If in doubt, choose this. Yucho is the only choice for your first bank account in Japan.

- Why: Most flexible screening, ATMs everywhere. Using the "Yucho Tetsuzuki App," you can open an account via face authentication without visiting a branch.

2. SBI Shinsei Bank

- Verdict: Best if you want to bank in English.

- Why: Their online banking supports English, making it safe for those not confident in Japanese. With their "Step Up Program," you can get free transfers to other banks if conditions are met.

3. Rakuten Bank

- Verdict: Best as a second bank after settling down.

- Why: Completely online, earns Rakuten Points. However, "Non-Residents (less than 6 months)" are explicitly not allowed to open an account. Wait for half a year.

🗣️ Real User Voices (2024-2025)

Here are the "Success Stories" and "Failures" from foreign residents in Japan, gathered from Reddit and X (Twitter).

✅ Success Stories (Good News)

Reddit User (2025) "Successfully opened a Yucho account in my first week. The app has English, and it was much less stressful than being bombarded with Japanese at the counter."

X User (Company Employee) "I showed my employee ID, and even SBI Shinsei Bank waived the '6-month rule'! If you are an employee, bringing proof of salary deposit is the strongest shortcut."

❌ Failures & Warnings (Bad News)

Reddit User (The Biggest Trap) "Rejected 3 times on the Yucho App. The reason? 'Katakana Name Input.' My Residence Card only has English, but the app demands perfect Katakana input. If you're not confident, going to the counter is faster."

Reddit User (Student) "I opened an account within 6 months, but there was a trap. Because it's treated as a 'Non-Resident Account,' when I tried to transfer money domestically (to pay rent), they tried to charge me 7,500 yen as an 'International Transfer' fee. Until 6 months pass, it's just a 'Cash Box'."

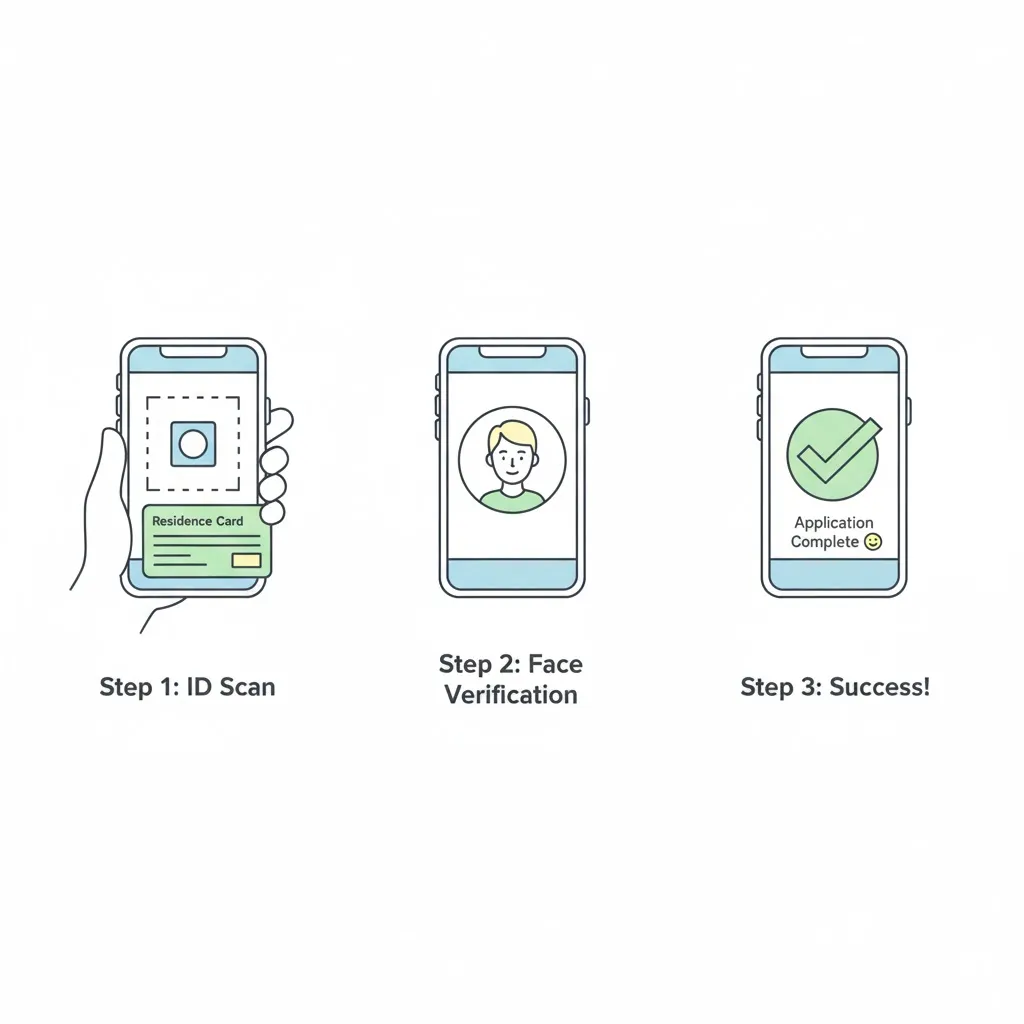

Practical Guide: Steps to Open a Yucho Account (Recommended Route)

Here is how to open an account using the "Yucho Tetsuzuki App," which has the highest success rate.

- Step 0: Preparation

- Residence Card (with address on back)

- Smartphone

- Japanese Phone Number (Must receive SMS)

- Step 1: Download the App

- Get "Yucho Tetsuzuki App" from the store. Select your language (English, Vietnamese, Chinese, etc.).

- Step 2: Identity Verification (eKYC)

- Follow the instructions to scan your Residence Card chip and take a selfie.

- Step 3: Information Input (The Hardest Part)

- Name: Input in Alphabet exactly as on your Residence Card.

- Kana: Input the Katakana pronunciation of your name accurately (e.g., SMITH → スミス). If this differs even by one character from what the bank expects, you will fail the screening.

- Step 4: Receive Cash Card

- Once screening is complete (approx. 1-2 weeks), the card will be sent via registered mail. You must be at home to receive it.

Next Step: What to Do After Opening (Avoid the Fee Trap)

Opening a bank account is not the "Goal," it's the "Start." However, many people fall into the "Fee Trap" here.

⚠️ Warning: Do NOT use the bank for "Transfers" in the first 6 months

Accounts opened within 6 months of arrival are legally treated as "Non-Resident Accounts." During this period, ATM withdrawals are free, but if you try to transfer money to another bank (e.g., for rent), it may be treated as an "International Transfer" even if it's domestic, costing thousands of yen (sometimes 7,500 yen!).

So, what should you do?

Solution: Use Wise

When sending money from your home country to Japan, or moving funds domestically, using a bank counter takes days and costs high fees. Wise allows for fast transfers with low fees, regardless of your "Non-Resident" status.

The smart foreigner's strategy is to use the newly opened bank account as a "place to receive salary" and leave transfers to Wise.

Don't Lose Money on Fees

Register for Wise to get a fee-free transfer coupon for up to 75,000 yen and avoid the bank's non-resident fees. Used by 16 million people worldwide.

Verdict: How Should You Open Your Account?

- Less than 6 months in Japan, student or unemployed: Open a Yucho account via the "Yucho Tetsuzuki App" — the most flexible screening in Japan. (Recommended)

- Less than 6 months, employed: Try SBI Shinsei Bank with your employee ID or contract; otherwise Yucho.

- More than 6 months: Add Rakuten Bank or another online bank as your second account.

- For all transfers in your first 6 months: Use Wise and treat the bank account as a salary receiver — not a transfer tool.

FAQ: Opening a Bank Account in Japan

Can a foreigner open a bank account in Japan within 6 months of arriving?

Yes. Japan Post Bank (Yucho) accepts newcomers with a visa of 3+ months remaining, and SBI Shinsei Bank can treat you as a "Resident" if you can prove employment in Japan. Note that accounts opened in your first 6 months are legally "non-resident" accounts with limited transfer functions.

What documents do I need to open a bank account in Japan?

Four items: your Residence Card with your current address printed on the back, a Japanese mobile number (090/080/070) in your own name, a Certificate of Residence (Juminhyo) for some counter applications, and a hanko (personal seal) for counter applications at Japan Post Bank. App-based applications usually skip the hanko.

Can I open a Japanese bank account without speaking Japanese?

Yes. The "Yucho Tetsuzuki App" supports English, Vietnamese, Chinese, and other languages, and SBI Shinsei Bank offers English online banking. Bank counters, however, operate mostly in Japanese.

Why was my Yucho application rejected?

The most common causes: your Katakana name input differs from what the bank expects (even by one character), less than 3 months remaining on your visa, your address input doesn't exactly match your Residence Card, or you already have a Yucho account (one per person). If the app rejects you repeatedly, apply at the counter instead.

Why are transfers from my new account so expensive?

Accounts opened within 6 months of arrival are treated as "Non-Resident Accounts." Domestic transfers can be processed as international transfers, costing up to ¥7,500 per transfer. Use the account to receive salary, and use a transfer service for moving money until the 6-month mark passes.

Summary: Start with "Yucho"

Opening a Japanese bank account is indeed a high hurdle for foreigners. However, if you follow this guide, you will succeed.

Your Action Plan:

- Today: Register your address at City Hall.

- Tomorrow: Get a phone number with Mobal SIM.

- Day After: Apply via "Yucho Tetsuzuki App" (Go to counter if it fails).

- After Opening: Register for Wise immediately to avoid high transfer fees.

With these 4 steps, your financial life in Japan will be free. Good luck!

Save this guide for later?

You might need this information again. Bookmark this page to access it anytime.

Get the free Moving in Japan checklist

A practical 14-day checklist for city hall, utilities, SIM, internet, and moving tasks.

Reading this in English?

Help improve English guides like this

If this guide helped but a phrase felt unnatural, your native check can make the next English article clearer for foreign residents in Japan.

🔗 Related Articles (Recommended)

- [10-Sec Check] HSP Visa Point Calculator: The Salary Strategy to Get Permanent Residency in 1 Year (2026)- Reccomended

- Residence Tax in Japan: Why Your Paycheck Shrinks in Year 2 & The "Leaving Japan" Trap- Reccomended

- Best Credit Card in Japan for Foreigners (2026): Rakuten vs EPOS vs Nexus- Reccomended

Disclaimer

※ The information in this article is accurate as of the time of writing. Laws and regulations may change, so please always check official sources for the latest information. We assume no liability for any damages resulting from the content of this article.

Related Articles

How to See a Doctor in Japan as a Foreign Resident (2026): Clinics, Costs, Pharmacies and After-Hours

Health Insurance & Pension Enrollment in Japan (2026): A Newcomer's First-Weeks Guide

Disaster Apps and Multilingual Emergency Info for Foreigners in Japan

Common Scams Targeting Foreigners in Japan and How to Avoid Them

Frequently Asked Questions

Q: Can a foreigner open a bank account in Japan within 6 months of arriving?

A: Yes. Japan Post Bank (Yucho) accepts newcomers with a visa of 3+ months remaining, and SBI Shinsei Bank can treat you as a Resident if you can prove employment in Japan. Accounts opened in your first 6 months are legally non-resident accounts with limited transfer functions.

Q: What documents do I need to open a bank account in Japan?

A: Four items: your Residence Card with your current address printed on the back, a Japanese mobile number (090/080/070) in your own name, a Certificate of Residence (Juminhyo) for some counter applications, and a hanko (personal seal) for counter applications at Japan Post Bank.

Q: Can I open a Japanese bank account without speaking Japanese?

A: Yes. The Yucho Tetsuzuki App supports English, Vietnamese, Chinese, and other languages, and SBI Shinsei Bank offers English online banking. Bank counters, however, operate mostly in Japanese.

Q: Why was my Yucho application rejected?

A: Common causes: your Katakana name input differs from what the bank expects, less than 3 months remaining on your visa, your address input doesn't exactly match your Residence Card, or you already have a Yucho account. If the app rejects you repeatedly, apply at the counter instead.

Q: Why are transfers from my new account so expensive?

A: Accounts opened within 6 months of arrival are treated as Non-Resident Accounts. Domestic transfers can be processed as international transfers, costing up to ¥7,500 per transfer. Use the account to receive salary and use a transfer service for moving money until the 6-month mark passes.