Can You Pay Initial Rental Costs with a Credit Card? Hacks to Split ¥500,000 and Screening Tips for Foreigners [2026]

CEO / Native Japanese Expert

Updated on: June 11, 2026

Housing & Daily Life

How this guide is checked

Updated against official, partner, and reviewed site evidence where available.

Last updated: June 11, 2026

Official or partner facts are separated from practical notes.

Prices, screening, documents, and rules can change.

Some next-step links may be monetized.

Needs review: Approval, visa/tax/legal, availability, and campaign terms are not guaranteed. Confirm on the official or partner page.

Send to Friends (Summary)

- •For foreigners who find Japanese rental initial costs (Deposit/Key Money) too expensive. We explain credit card acceptance, fee simulations for splitting a ¥500,000 payment, and 4 tips to pass the screening. Learn how to use Rakuten Card or Village House to survive moving costs.

Great for LINE / WhatsApp sharing

When renting an apartment in Japan, the first and biggest barrier you hit is the high "Initial Cost." Generally, it is said to require about 4.5 to 5 months' worth of rent. If your rent is ¥80,000, a massive sum of approx. ¥400,000 to ¥500,000 disappears in an instant.

"I don't have that much money in my Japanese bank account yet." "I'm scared to carry that much cash to the real estate agency."

For foreigners who feel this way, "Credit Card Payment" is a lifeline. To give you the conclusion first: Paying initial costs by card is "possible, but not available at all properties or agencies." However, if you know the right procedures, you can save your cash, earn points, and even split the payment over several months to lighten the burden.

In this article, we explain "Credit Card Payment Strategies" to smartly handle a ¥500,000 expense, along with tips for foreigners who might struggle with credit screening.

Earn over 5,000 points on initial costs

Get thousands of points with the sign-up campaign + 1% back on initial cost payments. Easily switch to installments later via the app.

Why Do Japanese Real Estate Agents Prefer "Cash"?

While checks and card payments are standard in many countries, "Bank Transfer" is still the mainstream method in Japan. The biggest reason is the "Transaction Fee" that the real estate company has to pay to the credit card company.

If you pay ¥500,000 by card, the real estate company loses about 3–5% of that sale (¥15,000–¥25,000) as a fee to the card issuer. Because this reduces their profit, many landlords and small real estate agencies dislike card payments.

However, recently, major chains (like Able and Apamanshop) and agents specializing in foreigners are increasingly marking properties as "Initial Cost Credit Card Payment OK." There are also many cases where "monthly rent cannot be paid by card, but the initial cost is OK," so it is important not to give up and ask.

3 Routes to Pay Initial Costs with a Credit Card

Here are the three main patterns for how you can actually make the payment.

1. Direct Card Payment in Store

This is just like shopping; you pay at the counter using a terminal with VISA, Mastercard, or JCB logos. This is adopted by many major brokerage chains, but be aware that American Express (AMEX) and Diners are sometimes refused due to higher fees.

2. Online Payment Link (SumaPAY, etc.)

In this pattern, the real estate company sends you a "Payment URL" via email. Systems like "Veritrans (SumaPAY)" are used, allowing you to complete the payment on your smartphone without visiting the store. This is extremely convenient if you want to finish payments before arriving in Japan.

3. BNPL Services (Buy Now Pay Later)

These are payment advancing services like "smooth" that you can use even if the real estate company doesn't support card payments. The service company pays the initial cost to the real estate agent on your behalf, and you pay the service company back in installments. While very convenient, be careful of the total payment amount, as fees often run around 18.0% annual interest.

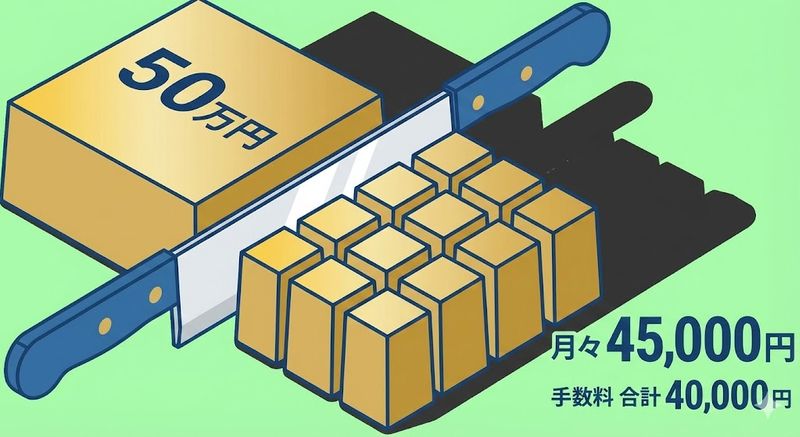

[Simulation] What Are the Fees if I Split ¥500,000 "Later"?

"Paying all at once is tough, but the fees for specialized BNPL services are too high..." In this case, a recommended hack is to pay the full amount with your existing credit card and then change it to "Installment Payment" (Bunkatsu-barai) later via your card company's app.

Let's look at the costs of splitting a ¥500,000 initial cost using a standard credit card (assuming an APR of around 14.75%).

| Payment Frequency | Monthly Payment | Total Fee (Interest) | Total Paid |

|---|---|---|---|

| One-time Payment | ¥500,000 | ¥0 | ¥500,000 |

| 3 Installments | Approx. ¥170,066 | Approx. ¥10,200 | ¥510,200 |

| 6 Installments | Approx. ¥86,733 | Approx. ¥20,400 | ¥520,400 |

| 12 Installments | Approx. ¥45,066 | Approx. ¥40,800 | ¥540,800 |

Calculated based on Rakuten Card's effective annual rate of 12.25%–14.75%.

Key Point: If you choose 12 installments (1 year), it costs about ¥40,000 in fees. However, if this allows you to keep ¥500,000 cash on hand, you could consider it a cheap "peace of mind" fee. Conversely, "Revolving Payment (Ribobarai)" carries the risk of extending the repayment period and ballooning fees, so be sure to choose "Installment Payment" (split by number of times).

4 Defensive Measures for Foreigners to Pass Screening with Card Payment

When foreign tenants hope to pay by card, specific troubles tend to occur. Prepare the following four points in advance.

1. Breaking Through the Limit Wall

Credit cards made immediately after arriving in Japan often have a usage limit set to ¥200,000–¥300,000. This isn't enough to pay a ¥500,000 initial cost. Solution: Call your card company and apply for a "Temporary limit increase" for moving expenses. If you pass the screening, your limit can be raised to something like ¥1 million for just one month.

2. Watch the "Balance" on Debit Cards

If you use a Debit Card instead of a Credit Card, the full amount is deducted from your bank account the moment you pay. If your balance is short by even ¥1, you will get an "Approval Error" and face an awkward moment at the real estate counter. Make sure to deposit money the day before.

3. Avoid "No Foreigners" Properties

Fundamentally, before worrying about card payments, you can't contract a property unless it accepts foreign tenants. To save time, taking a shortcut by using agents or guarantor companies accustomed to foreigners, such as GaijinPot Housing Service or GTN, is recommended.

4. Have a "Backup" for Payment Errors

Credit cards issued overseas are prone to security locks on Japanese payment systems. "VISA failed but Mastercard worked" is a common occurrence, so always bring two cards from different brands, or in the worst case, be prepared to withdraw cash from a convenience store ATM.

Recommended Services to Reduce Initial Costs or Pay by Card

Finally, here are two services perfect for foreigners who want to reduce the burden of initial costs.

Rakuten Card

A must-have card for life in Japan.

- No annual fee forever, and easy for foreigners to apply for (site language depends, but they have a track record of approving foreigners).

- If you pay ¥500,000 in initial costs, you get 5,000 points (worth ¥5,000) back.

- The app is user-friendly, and changing to "installments later" after payment is simple.

Village House

A smart choice for those who "don't want to pay initial costs in the first place."

- ¥0 Deposit, ¥0 Key Money, ¥0 Brokerage Fee, ¥0 Renewal Fee.

- Since the initial cost is only a few tens of thousands of yen (like pro-rated rent for the current month), you don't even need to worry about installment interest rates.

- Occupation is not questioned, and the screening is very flexible for foreigners.

Instead of 'splitting' costs, make them ¥0

¥0 Deposit, Key Money, Fee, and Renewal Fee. Screening is foreigner-friendly with no occupation requirements.

Frequently Asked Questions (FAQ)

Can I pay the Application Fee by card too?

In most cases, application fees (usually around ¥10,000–¥30,000) or earnest money must be paid via "Cash or Bank Transfer only." Card payments are generally used for the main contract payment (the large amount).

Does paying by card make rent negotiation harder?

Yes, that is a possibility. Since the real estate company is bearing the transaction fee, they often say, "If you pay by card, we cannot offer a discount."

Can I pay with a friend's credit card?

Absolutely NOT. The name on the rental contract and the name on the credit card must match. If it is a family card under the name of the contractor (or a family member living together), it may be accepted.

Summary

Initial rental costs in Japan are high, but by utilizing credit cards, you can enjoy the benefits of "earning points," "deferring payment," and "paying in installments."

- First, get a Japanese card like the Rakuten Card.

- Ask the real estate company right away, "Is card payment possible for initial costs?"

- If your limit is insufficient, apply for a "Temporary Limit Increase."

- If it still feels too expensive, choose a zero-initial-cost property like Village House.

Use these steps to start your new life without financial strain.

Save this guide for later?

You might need this information again. Bookmark this page to access it anytime.

Get the free Moving in Japan checklist

A practical 14-day checklist for city hall, utilities, SIM, internet, and moving tasks.

Reading this in English?

Help improve English guides like this

If this guide helped but a phrase felt unnatural, your native check can make the next English article clearer for foreign residents in Japan.

Disclaimer

※ The information in this article is accurate as of the time of writing. Laws and regulations may change, so please always check official sources for the latest information. We assume no liability for any damages resulting from the content of this article.

Related Articles

Frequently Asked Questions

Q: Can I pay Japanese apartment initial costs (deposit, key money, agency fee) by credit card?

A: Some agencies accept credit cards for initial costs, but many traditional agencies and direct landlords still require bank transfer. Check explicitly with the agency before applying. Online-focused agencies like Best-Estate and UR Housing are more likely to accept card payment.

Q: Which Japanese credit cards are easiest for foreigners to get to pay rental costs?

A: Rakuten Card is the most accessible — no Japanese credit history required, approved for most Residence Card holders. GTN Card is specifically designed for foreigners with no credit history. Both are free annual-fee cards useful for splitting large initial costs.

Q: Can I split the initial rental costs into installments with a credit card?

A: You can use a revolving credit (リボ払い, ribo harai) option on your credit card to spread payments, but this incurs high interest (typically 15–18% annually). A better strategy is to pay in full and then time your application to maximize credit card sign-up bonuses or points campaigns.

Q: What is the "Foreign Credit Card Trap" for paying rent in Japan?

A: Some landlords charge an additional processing fee (3–5%) for credit card payments. If you use a foreign card with a foreign transaction fee (1.5–3%) on top, you could pay 5–8% extra. Use a Japanese card (Rakuten Card has no foreign transaction fee) or Wise to avoid stacking fees.

Q: Does Village House accept credit card for initial costs?

A: Village House typically accepts bank transfer for their minimal initial costs (usually just a small administrative fee plus first month's rent). Credit card acceptance varies by property — check directly with Village House when applying.